Hurricane Season:

The One Insurance Step Most Florida Landlords Skip

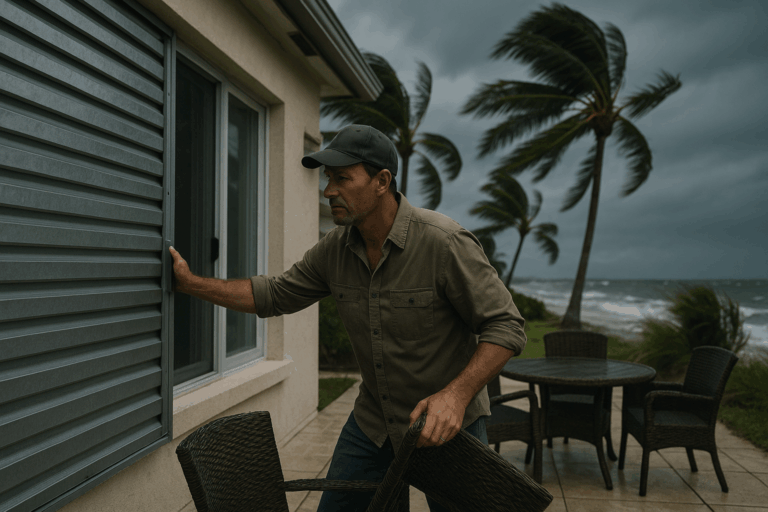

The Atlantic hurricane season is officially underway. While early forecasts suggest a potentially average or slightly below-average storm season due to El Niño patterns, history has taught Florida real estate investors a brutal lesson: it only takes one storm to cause catastrophic damage.

However, the real danger for landlords isn’t just the wind or the rain—it’s the insurance battle that follows.

Recent data from past major storms like Hurricanes Milton, Helene, and Debby revealed a shocking trend in Florida. During Hurricane Milton, 34.8% of claims were closed without payment. For Hurricane Helene, that number jumped to 60%, and a staggering 68% of residential claims for Hurricane Debby were completely denied.

The number one preventable reason behind these denials? Insufficient documentation of the property’s pre-storm condition.

The “Deductible Trap” and How Insurers Defend Denials

Many independent landlords don’t realize that their hurricane deductible is calculated as a percentage of the home’s total insured value, not a flat fee. If your rental property is insured for $400,000 and you have a 5% hurricane deductible, you are responsible for the first $20,000 out of pocket.

When a landlord files a claim for damages that fall right around or above that threshold, insurance adjusters look for any reason to deny it. Their favorite argument? “This damage was pre-existing.”

Without clear, time-stamped evidence proving the exact state of your roof, gutters, fences, and interior rooms right before the storm made landfall, it becomes your word against theirs. In court, the insurance company usually wins that argument.

The 1-Hour Preventive Fix Every Landlord Needs to Do Now

The most frustrating part of this statistic is that protecting yourself is completely free and takes less than an afternoon. Before the next tropical system threatens the Florida coast, you or your management team must complete a Pre-Storm Documentation Protocol:

-

Comprehensive Video Walkthrough: Walk the entire exterior and interior of the property. Film the roof line, the siding, windows, and every room. Ensure your camera or phone has the date and location timestamps enabled.

-

Document Property Maintenance: Take specific photos of trimmed trees, cleared gutters, and secure fences. Florida insurers are increasingly denying claims by arguing the landlord failed to maintain the property. A photo proving your trees were trimmed undercuts this defense immediately.

-

Archive the Records Digitally: Do not leave these photos on a single phone or computer. Save them to a secure cloud-based property drive so they can be pulled instantly if a claims adjuster requests them.

How Bahia Property Management Shields Your Investment

Managing hurricane compliance, tenant communications, and high-stakes insurance documentation is an exhausting, full-time job.

At Bahia Property Management, we handle the heavy lifting to ensure your asset is fully protected before, during, and after a storm:

-

Standardized Pre-Season Inspections: We systematically document the exterior and interior baseline conditions of your property with photographic evidence.

-

Proactive Maintenance Coordination: Our certified vendor network ensures trees are trimmed and gutters are cleared to nullify insurance negligence arguments.

-

Post-Storm Emergency Response: If a storm hits, our team is on the ground immediately to document damage, coordinate emergency tarping, and assist in providing the ironclad paperwork your insurance company demands to pay out your claim.

🌪️ Don’t Let a Deductible Trap Destroy Your Cash Flow

When the next storm rolls into Tampa, Orlando, or Miami, will your property’s pre-storm condition be fully documented, or will you face a 60% chance of a denied claim? Protect your asset with a professional team that knows Florida real estate laws and insurance protocols inside and out.